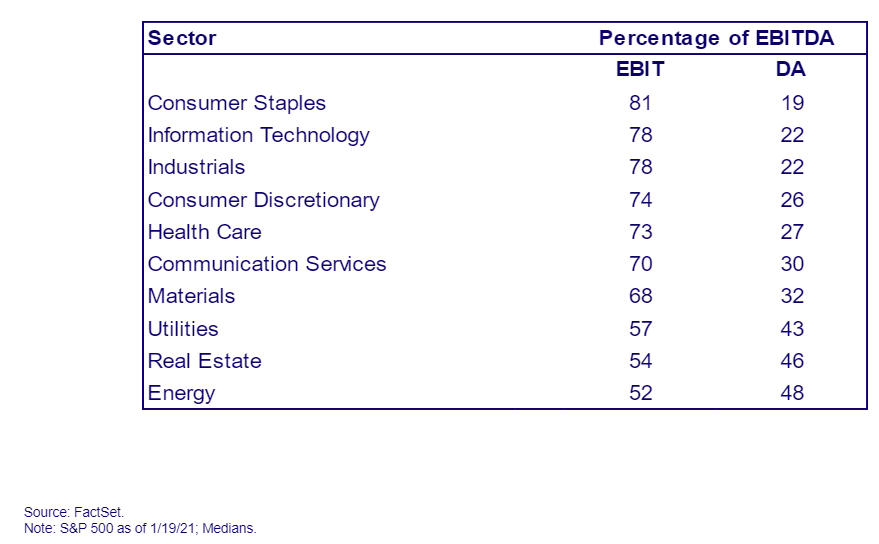

Enterprise Value is the total value of a firm and is defined as equity value (market cap) + debt (long-term and short-term) + preferred stock + minority interest – cash and cash equivalents. Earnings before interest, taxes, depreciation and amortization (EBITDA) is simply operating income (EBIT) plus depreciation and amortization. While many analysts on Wall-Street use EV/EBITDA probably because the ease of its computation and the reasoning that EBITDA approximate Free Cash Flow which is wrong (we will see later why), I have also been guilty of using this metric many times before. First, EV/EBITDA can be used only in industries where depreciation and amortization expense are low (for instance, technology) and is not particularly useful in industries with high D&A expense such as Telecommunication, Energy, etc. Professor Michael Maubousin of Columbia Business School pointed out in a recent Tweet the degree to which EV/EBITDA multiple is used “When I see people throw around EV/EBITDA multiples, I always wonder if they are aware of how much is EBIT, how much is DA, and why it matters”

Also, Warren Buffet dislikes the use of EBITDA and said once “Does management think the tooth fairy pays for capital expenditures?” EBITDA is a poor proxy for Free Cash Flow (FCFF) because it ignores the cash taxes paid by the firm as well as the investments in working and fixed capital. So what is better than EV/EBITDA? Two measures I like to use are Enterprise Value to Operating Income (EV/EBIT) which is called the Acquirer’s Multiple by Tobias Carlisle and reflect both depreciation and amortization and Enterprise Value to Free Cash Flow to Firm (EV/FCFF) since FCFF reflects cash available to debt and shareholders alike after taking into consideration non-cash charges, after tax cost of interest, capital expenditures and working capital and can be simply computed as cash flow from operations + after-tax cost if interest – fixed capital investments: FCFF= CFO + Int (1-t) – Capex. The lower the EV/EBIT or EV/FCFF, the cheaper a stock is. You can inverse EV/EBIT and EV/FCFF to EBIT/EV and FCFF/EV to get an earnings yield (part of Joel Greenblatt’s magic formula in his little book that beats the market) or free cash flow Yield which are better measures than the widely used earnings yield (E/P) ratio. The higher the yield, the better the investment! (FCFF best represents a company’s performance and is less prone to management manipulation than earnings).