In this post, I want to discuss what is stock-based compensation (also known as share-based compensation or equity compensation) and why it is a controversial subject when it comes to calculating the Free Cash Flow of any firm. First, what is stock-based compensation? As the name suggests, It basically a form of compensation offered by firms across all industries, but most notably the tech industry where it aims to attract and retain talented employees. All employees get cash compensation in the form of a salary that is paid either monthly, or biweekly plus a bonus that is paid quarterly, semi-annually, or annually. However, stock compensation is a stock reward (equity ownership) to employees, directors, executives, etc. which serves the purpose of motivating them beyond their salaries and bonuses and closely tie their interests with those of shareholders since the employees’ compensation is linked to the company’s stock performance. The stocks are vested over a period (usually years) meaning that these new stocks will not be issued immediately, but rather after some time. What happens usually is that when those stocks are issued after the vesting period is over, shareholders’ ownership will be diluted! In other words, shareholders will have less equity in the business. Now, what do most companies do when reporting their numbers? Most companies nowadays report Non-GAAP numbers alongside their GAAP numbers so they make a few adjustments by adding back many non-cash charges such as depreciation and amortisation which make sense and other adjustments that don’t make sense such as stock-based compensation! Under GAAP, companies have to expense stock-based compensation in the income statement. Most companies expense different portions of this compensation in their cost of sales and operating expenses. However, Companies and analysts often argue that stock-based compensation is non-cash and thus, should be added back when calculating free cash flow. This is wrong! Why? I quote Warren Buffett here “If options aren’t a form of compensation, what are they? If compensation isn’t an expense, what is it?”. Let me give you an example, imagine I own a portfolio of properties worth 100 million USD and I hire someone to manage this portfolio, but instead of paying them cash (salary), I agree to give them 1% ownership in my properties for every year they manage the portfolio. Now, I want to sell my portfolio of properties after 5 years! What is my ownership percentage? It’s 95% now instead of 100%!! This is what dilution means!

I will walk you through a specific example concerning PayPal Holdings Inc. which is an American multinational financial technology company operating an online payments system in the majority of countries that support online money transfers and serves as an electronic alternative to traditional paper methods such as checks and money orders. Let us start looking at GAAP and Non-GAAP numbers reported by the company. We will focus on three things.

1) GAAP Operating Income (EBIT) vs Non-GAAP Operating Income (Adjusted EBIT). 2) GAAP Earnings Per Share (EPS) vs Non-GAAP Earnings Per Share (Adjusted EPS). 3) Correct way to calculate Free Cash Flow (FCF) vs Adjusted Free Cash (Adjusted FCF): Note that both are Non-GAAP numbers!

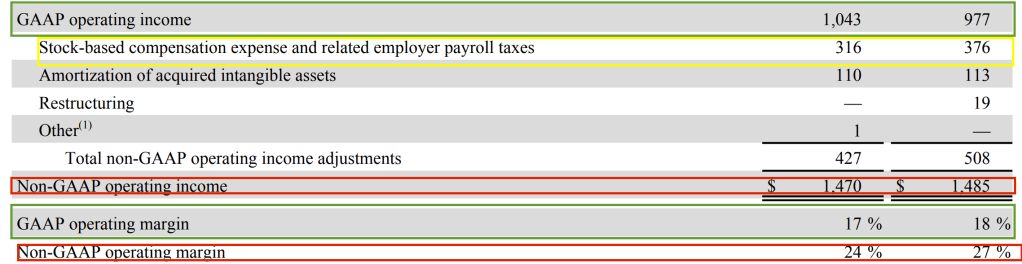

1- Let us start by looking at GAAP Operating Income (EBIT) vs Non-GAAP Operating Income (Adjusted EBIT) as reported by Paypal. The ones highlighted in green are GAAP numbers, Yellow is the stock-based compensation adjustment and red for the Non-GAAP adjusted numbers. We can see that the Non-GAAP Operating Income and Operating Margin which were $1470 and 24% respectively for the third quarter of 2021 vs the GAAP Operating Income and Operating Margin of $1043 and %17 respectively for the same reporting period.

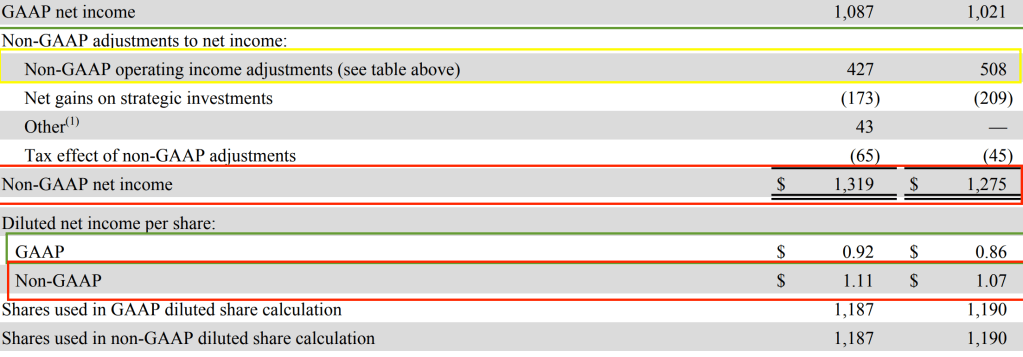

2)- We will compare GAAP Earnings Per Share (EPS) vs Non-GAAP Earnings Per Share (Adjusted EPS) as reported by Paypal. We can see here again that the Non-GAAP adjustments highlighted in yellow artificially boosted Net Income Per Share from $0.92 to $1.11 for the quarter of 2021.

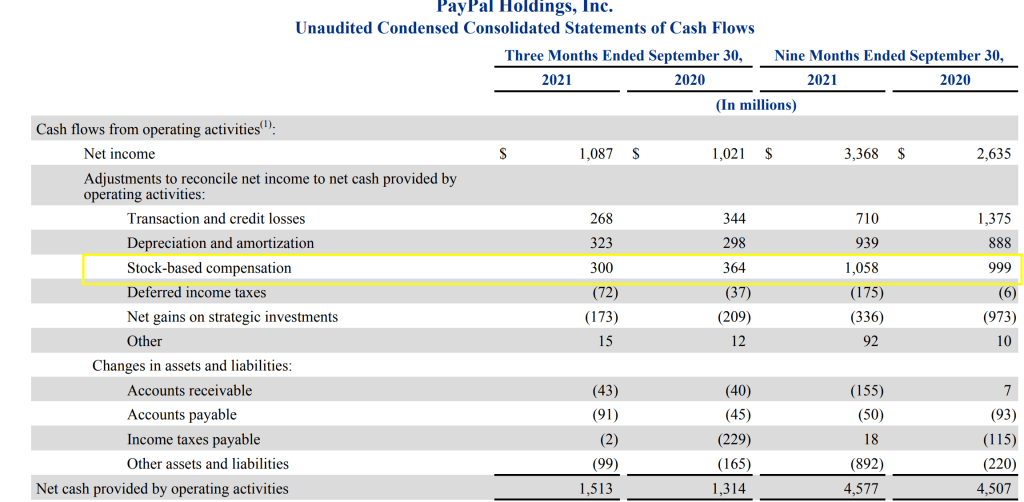

3- If you look at the adjustments the company made to arrive at the Net Cash Provided by Operating Activities (CFO), you can see that the numbers, in this case, are inflated for the 3rd quarter of 2021 ($1.11 vs $0.92). This misrepresentation led to the overstatement of the company’s Free Cash Flow (FCF). If CFO is overstated, then FCF will be too! Most analysts fall into this trap also by using adjusted numbers given by companies which include stock-based compensation! The simple solution is to exclude stock-based from your calculations to arrive at FCF. If you do that for 2020 and 2021, you will see that CFO is $1213 instead of $1513 for the 3rd quarter of 2021 and $3519 instead of $4577 for the first 9 months of 2021 as shown below:

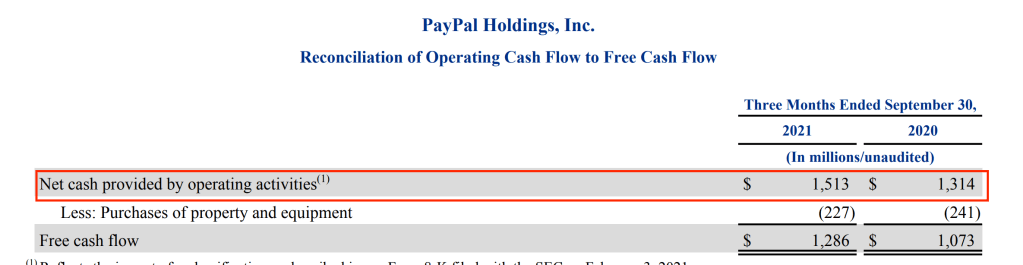

So now the final piece will include Free Cash Flow Calculation with and without adding back stock-based compensation. Let us assume for simplicity purposes that FCF can be calculated excluding after-tax interest cost which means that the formula we are using is the following: CFO – Capex. Below, You can see the numbers reported by PayPal for the third quarter of 2021. If you use CFO reported by the company which is adjusted for stock-based compensation you will get $1286 FCF for the 3rd quarter,2021. The right approach which includes stock-based compensation as an expense will yield FCF of $986 instead of the reported $1286 and that’s only for one quarter!!

Conclusion: Companies report both GAAP and Non-GAAP numbers in their reports. Companies also provide guidance regarding next quarter’s or year’s revenues, Non-GAAP margins and Non-GAAP EPS. Most analysts forecast using Non-GAAP margins and Non-GAAP EPS without taking into account adjustments made by the company! and thus many companies will look cheap on the surface (using consensus estimates), whereas, in reality, they are much more expensive. Paypal might be a great business and I am not saying whether it’s overvalued or undervalued since I haven’t done proper work on the company. However, the whole point here is to highlight a very well spread phenomenon (especially in tech) which requires thoughtful analysts and investors to be careful of stock-based compensation and other forms of non-sense adjustments before recommending or investing their or their clients’ hard-earned money into what is perceived to be a cheap stock.